Federal vs. private student loans: Best repayment options

- TitanPrep Official

- May 13

- 9 min read

Many borrowers refinance their federal student loans into private ones without realizing they are permanently giving up protections that took decades to build into law. That single decision can eliminate access to income-driven repayment, Public Service Loan Forgiveness, and emergency relief options. With the federal repayment landscape shifting significantly in 2026, understanding the difference between federal and private loans is no longer just useful background knowledge. It is the foundation of every smart repayment decision you will make.

Table of Contents

Federal vs. private student loans: What’s the real difference?

Repayment options and protections: How federal and private loans stack up

The 2026 landscape: New federal repayment programs and key eligibility rules

Edge-case pitfalls: Why refinancing can cost you federal benefits

Get personalized help for your loan type and repayment options

Key Takeaways

Point | Details |

Federal vs private loan basics | Federal loans are government-managed with standardized terms; private loans are lender-created and vary widely. |

Repayment and relief differences | Federal loans offer income-driven repayment and forgiveness, while private loans typically lack these protections. |

Upcoming federal rule changes | Starting July 1, 2026, federal repayment options shift to new IDR and RAP pathways for new borrowers. |

Risks of refinancing | Refinancing federal loans into private formats means losing federal repayment and relief benefits permanently. |

Strategy for complex cases | Always identify your loan type and maximize federal options before considering private solutions. |

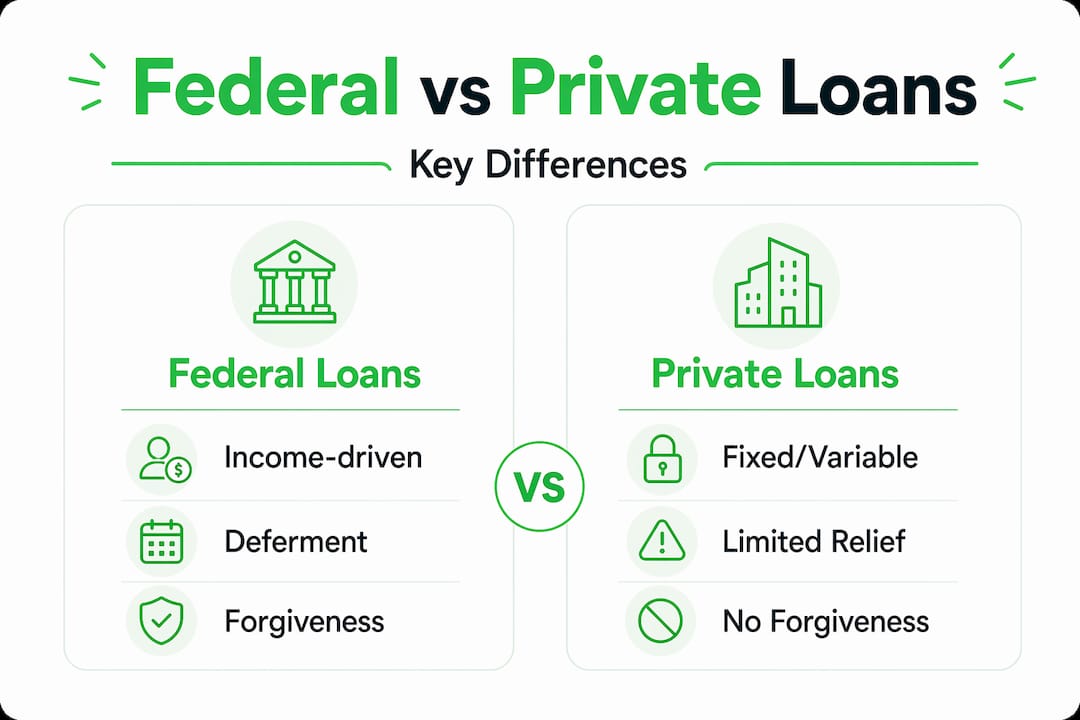

Federal vs. private student loans: What’s the real difference?

The gap between federal and private student loans is not just about interest rates or who you write your check to. It is a structural difference that shapes every repayment option, relief program, and protection available to you.

Federal Student Aid manages federal student loans, including Direct Loans and PLUS Loans, which are standardized by federal law. Private student loans, on the other hand, are contracts made between you and a bank or lender, with terms that vary widely from one lender to the next. This distinction directly affects your eligibility for relief and repayment support in ways that matter enormously over the life of your loan.

Here is a quick comparison to ground the differences:

Feature | Federal loans | Private loans |

Administered by | U.S. Department of Education | Banks, credit unions, lenders |

Interest rates | Fixed, set by Congress | Fixed or variable, set by lender |

Income-driven repayment | Yes | No |

Loan forgiveness programs | Yes (PSLF, IDR forgiveness) | No |

Deferment and forbearance | Standardized | Varies by lender |

Eligibility check | Lender-specific |

Key characteristics of each loan type:

Federal loans are tied to your enrollment status, financial need (for subsidized loans), and federal eligibility rules

Private loans are credit-based products, meaning your approval and rate depend on your credit score and income

Federal loans carry fixed interest rates that Congress sets annually

Private loans may carry variable rates that can increase over time

Federal loans automatically qualify you for a range of repayment programs; private loans do not

Understanding which type of loan you have is the starting point for building a smart repayment strategy. Review your options in our federal loan forgiveness guide and learn the basics of constructing repayment plans that actually fit your financial situation.

Repayment options and protections: How federal and private loans stack up

Understanding these core structural differences, you will see how repayment and relief options diverge sharply between federal and private loans. The gap is not subtle. In many situations, it can mean the difference between an affordable monthly payment and financial hardship.

Federal loans offer borrowers deferment and forbearance as standardized temporary relief options. Deferment lets you pause payments without interest accruing on subsidized loans. Forbearance pauses payments too, but interest accrues on all loan types during that period, which means your balance grows. These protections are generally not available on private loans in the same standardized way, meaning a private lender may or may not help you, and the terms are entirely up to them.

Income-driven repayment, commonly called IDR, is a federal-only pathway. Under IDR plans, your monthly payment is calculated as a percentage of your discretionary income, meaning it adjusts when your income changes. Federal loans offer IDR and forgiveness pathways while private loans typically do not provide access to those programs at all.

Here is a side-by-side breakdown of key protections:

Protection | Federal loans | Private loans |

IDR repayment | Available | Not available |

Loan forgiveness (PSLF, IDR) | Available | Not available |

Standardized deferment | Yes | Rarely |

Forbearance options | Standardized | Varies |

Discharge for disability | Yes (Total and Permanent Disability) | Rare, lender-specific |

Discharge for school closure | Yes | Rare |

Additional points to keep in mind:

Private lenders may offer short-term hardship forbearance programs, but they are not required to, and terms differ significantly

Some private lenders offer refinancing options or interest rate reductions for on-time payments, but these are perks, not legal protections

If you have both federal and private loans, you need to track them separately because the rules that apply to one do not cross over to the other

Pro Tip: If you are unsure whether your payment plan is the most affordable option available to you, review the step-by-step payment lowering process before making any changes. You may qualify for a lower payment right now without taking on any risk.

For the most current relief programs and policy updates, check the latest forgiveness guidance to make sure you are not missing an option you already qualify for.

The 2026 landscape: New federal repayment programs and key eligibility rules

As federal rules evolve, here is what you need to know about the coming 2026 changes and what they mean for your repayment journey. The stakes are real. The timing of when you borrowed and whether your loans are federal will determine which programs you can access going forward.

Starting July 1, 2026, the federal income-driven repayment landscape is changing significantly. According to TICAS, new borrowers after that date are expected to have a simplified set of IDR choices, with the Repayment Assistance Plan (RAP) highlighted as the primary new income-driven option available.

What does this mean in practical terms?

New borrowers (after July 1, 2026) will likely be guided toward the Repayment Assistance Plan and a streamlined set of IDR options

Existing borrowers may retain access to older plans, but access to specific plans depends on your borrowing date and enrollment history

Private loan borrowers will not be affected by any of these changes because private loans are never eligible for federal IDR programs

Federal loan borrowers who have been on IDR plans should confirm their current plan status and whether it remains available to them after the transition

The difference in access is significant. Borrowers with federal loans will have a clear set of pathways to explore. Borrowers with private loans will need to negotiate directly with their lenders, with no federal safety net to fall back on.

Pro Tip: If you are approaching your repayment period or considering a refinance in 2026, now is the time to map out your federal eligibility before making any moves. Review the full 2026 relief rule changes so you understand exactly what is available based on when you borrowed.

One data point that puts the scale in perspective: as of early 2026, more than 40 million Americans hold federal student loan debt, and a large portion are still not enrolled in the IDR plan that best fits their income. The 2026 changes are designed to simplify that process, but you need federal loans to benefit. Visit our forgiveness guide to check your eligibility now.

Edge-case pitfalls: Why refinancing can cost you federal benefits

The final major difference comes when considering how to optimize your loans, especially in complex situations and edge cases. Refinancing sounds appealing when a private lender offers you a lower interest rate. But before you sign anything, you need to understand exactly what you are giving up.

When you refinance federal loans with a private lender, those loans become private loans and you permanently lose your federal benefits. There is no way to reverse that process. The IDR options, PSLF eligibility, deferment protections, and discharge programs you had access to before are gone the moment you refinance into a private product.

Here is a step-by-step process to protect yourself before considering any refinancing decision:

Identify your loan types. Log in to studentaid.gov and pull your complete federal loan summary. Know exactly which of your loans are federal and which are already private.

Check your IDR eligibility. Before you refinance, confirm whether you qualify for an income-driven repayment plan that could lower your payment more than a private refinance would.

Assess your PSLF eligibility. If you work for a qualifying employer (government or nonprofit), you may be on track for loan forgiveness after 10 years of payments. Refinancing would immediately disqualify you.

Evaluate your income stability. Federal loans protect you if your income drops. Private refinancing provides no safety net. If your income could change, keeping federal protections is worth more than a slightly lower rate.

Get your paperwork in order. If you decide to keep your federal loans and pursue relief, make sure your repayment plan applications, employment certifications, and income documentation are accurate and up to date.

“If you refinance federal loans into private loans, you lose access to federal repayment plans, forgiveness programs, and other protections. This is a permanent change that cannot be undone.”

This is not a hypothetical risk. Many borrowers refinanced during low-rate periods and later found themselves ineligible for relief programs they would have qualified for otherwise. The lesson is simple: always verify your federal eligibility before you take any action that converts federal loans into private ones. Use the guidance on constructing optimal repayment plans to see whether your current federal setup can be improved before you consider a private lender.

What most guides miss about federal vs. private loans

Most articles on this topic treat the federal versus private question as a one-time decision you make when you first borrow. That framing misses the point entirely. The more important question is this: what are you eligible for right now, and are you using it?

Here is the practical decision rule that too few borrowers actually follow: start with your loan type, then build your repayment strategy around the federal options you may already qualify for, including IDR, relief, and forgiveness programs, because private loans typically will not connect to those federal mechanics no matter how they are structured.

The borrowers who get into trouble are not always the ones with the highest balances. They are often the ones who refinanced into private loans during a period of low rates, thinking they were being financially smart, and then lost IDR access when their income dropped or their employer qualified them for PSLF. They saved a fraction of a percent in interest and gave up tens of thousands in potential forgiveness.

Strategic borrowers do the opposite. They treat federal loan benefits as the floor they build everything on top of. They confirm their PSLF eligibility before accepting a new job. They enroll in the IDR plan that fits their income now and recheck it every year during annual recertification. They look at private refinancing only after they have verified that none of their federal protections would apply to them in any realistic future scenario.

The truth is, private refinancing makes sense for a narrow set of borrowers: those with high-income stability, no PSLF-eligible employment, no IDR benefit, and a meaningful interest rate gap that justifies the trade-off. For everyone else, the federal system offers more protection than most borrowers realize. The key is learning to use it.

Get personalized help for your loan type and repayment options

As you sharpen your strategy, these resources offer next-step support for every borrower navigating federal and private loans. Whether you are just starting to understand your options or you are preparing for the 2026 IDR changes, having the right support makes a real difference.

At TitanPrep, we help borrowers organize and submit the paperwork required for federal programs like IDR, PSLF, and borrower discharge options. We track deadlines, store documents securely, and help you stay compliant with program requirements so nothing falls through the cracks. If you are ready to take action, get student loan help tailored to your specific situation. Download our forgiveness guide to understand exactly which federal programs you may qualify for. And stay current with the student loan updates that matter most as the 2026 changes roll out. TitanPrep does not guarantee forgiveness or specific outcomes. Eligibility is determined by the U.S. Department of Education or your loan servicer.

Frequently asked questions

How can I tell if my student loan is federal or private?

Federal loans are listed on the Federal Student Aid website at studentaid.gov; private loans come from banks or other lenders and do not appear there.

Can private student loans ever qualify for federal forgiveness or income-driven repayment?

No, private loans do not qualify for federal forgiveness or income-driven repayment programs; only federal loans can access those options.

Will refinancing federal loans with a private lender affect my protections?

Yes, refinancing federal loans makes them private and you permanently lose federal benefits such as IDR, forgiveness, and relief programs.

What changes are coming to federal repayment plans in 2026?

After July 1, 2026, new borrowers will access simplified income-driven repayment choices and the Repayment Assistance Plan as the primary new IDR option.

Are deferment and forbearance options different for federal versus private loans?

Federal loans offer standardized deferment and forbearance, but private loans may offer less relief and terms vary significantly by lender.

Recommended

Comments