Student Loan Cancellation: Relief, Rules, and 2026 Changes

- TitanPrep Official

- May 6

- 9 min read

Many borrowers spend years chasing loan forgiveness without realizing a faster option may already apply to their situation. Loan cancellation is a separate pathway that can eliminate your federal student loan balance immediately, without requiring decades of payments or years of public service. If your school misled you, closed while you were enrolled, or if you’ve experienced a severe disability, you could qualify for discharge right now. This article breaks down exactly what cancellation means, which programs are available, how they compare to forgiveness, and what the latest 2026 rule changes mean for you.

Table of Contents

Key Takeaways

Point | Details |

Loan cancellation delivers immediate relief | Cancellation eliminates student loan debt for qualifying events like disability or school misconduct. |

Key federal programs explained | Borrower Defense, Closed School, Disability, and Death Discharge provide specific cancellation pathways. |

Forgiveness is not cancellation | Forgiveness rewards long-term service or consistent payments, while cancellation addresses urgent hardships. |

New rules impact eligibility | 2026 updates narrow public service employer criteria and make IDR forgiveness taxable after 2025. |

Avoid mistakes to preserve relief | Consolidating or refinancing federal loans may void cancellation eligibility; always check before acting. |

Defining loan cancellation: What it means and how it differs from forgiveness

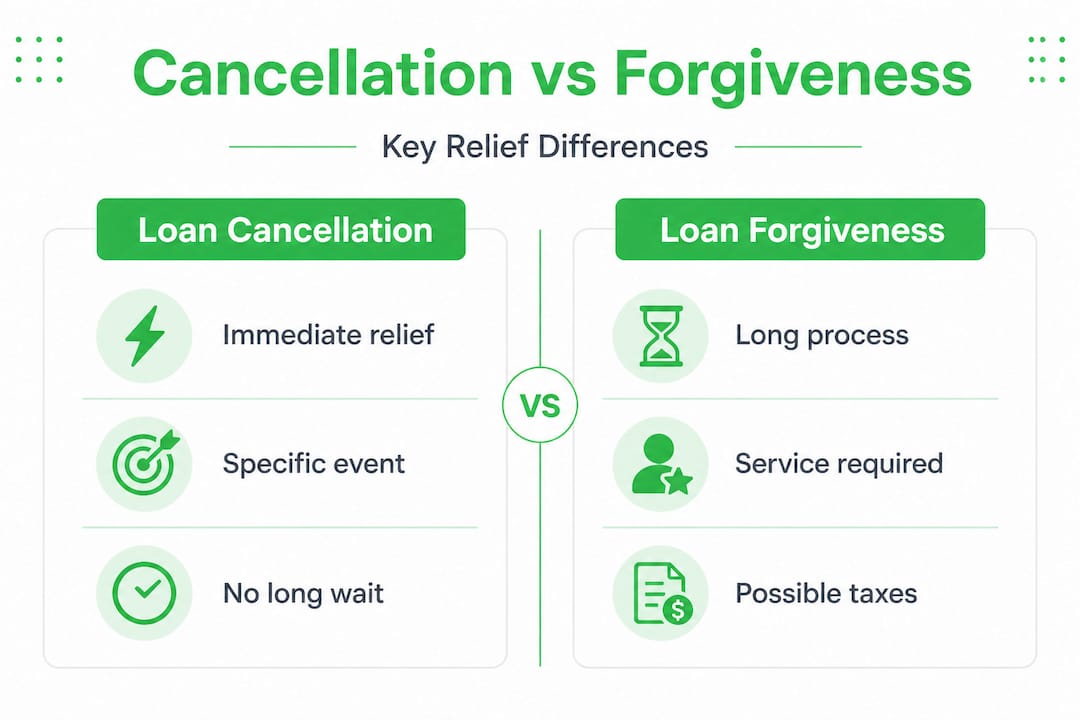

Most borrowers use “cancellation” and “forgiveness” interchangeably. That’s understandable, but the two terms describe very different processes with very different timelines.

Loan cancellation refers to discharge programs where your repayment obligation is eliminated because of a specific qualifying event, such as school misconduct, school closure, disability, or death. Forgiveness, on the other hand, is something you earn over time through public service or long-term repayment under an income-driven plan.

Think of it this way. Cancellation responds to something that already happened to you. Forgiveness rewards something you’ve done over many years.

Here’s a quick side-by-side to make this concrete:

Feature | Loan cancellation | Loan forgiveness |

Timeline to relief | Immediate (upon qualification) | 10 to 30 years |

Based on | Qualifying event | Service or payment history |

Examples | School closure, disability, fraud | PSLF, IDR, Teacher Forgiveness |

Application type | Discharge application | Ongoing program enrollment |

Partial or full relief | Can be either | Usually full after threshold |

Why does this distinction matter? Because many borrowers who qualify for cancellation spend years enrolled in forgiveness programs instead, making payments they didn’t need to make. Knowing the difference can save you real money and real time.

Common qualifying reasons for loan cancellation include:

School misconduct or misrepresentation (Borrower Defense to Repayment)

School closure while you were enrolled or shortly after

Total and permanent disability preventing you from working

Death of the borrower or, in some cases, the parent

You can learn more about how these programs compare by reviewing this student loan forgiveness program overview, or by checking the StudentAid.gov forgiveness article for official program descriptions.

With definitions clarified, let’s examine the specific programs available for loan cancellation relief.

Federal loan cancellation programs: Who qualifies and how

Federal loan cancellation is not a single program. It’s a collection of separate discharge options, each designed for a different qualifying situation. Understanding which one applies to you is the first step toward getting real relief.

Key cancellation programs include Borrower Defense to Repayment, Closed School Discharge, Total and Permanent Disability Discharge, and Death Discharge, each with its own eligibility rules and application process.

Here’s a breakdown of each:

Program | Who qualifies | Relief type |

Borrower Defense to Repayment | Victims of school misrepresentation or breach of contract | Full or partial discharge |

Closed School Discharge | Enrolled when school closed, or withdrew within 180 days | Full discharge |

TPD Discharge | Unable to work due to total and permanent disability | Full discharge |

Death Discharge | Borrower or parent PLUS borrower dies | Full discharge |

How each program works in practice:

Borrower Defense to Repayment. This program covers borrowers whose schools used deceptive tactics to recruit them, made false claims about job placement rates, or violated state laws. You submit a Borrower Defense application detailing the misconduct, the Department of Education reviews your evidence along with the school’s response, and a full or partial discharge is granted if the claim is proven. This process can take years, and you may be placed in forbearance while you wait.

Closed School Discharge. If your school closed while you were still attending, or within 180 days of your withdrawal, you may qualify. In many cases, this discharge now happens automatically. You don’t need to enroll in a teach-out program or transfer credits to another institution to qualify. Learn more about this in our closed school discharge guide.

Total and Permanent Disability (TPD) Discharge. This program requires medical documentation confirming you cannot engage in substantial gainful activity due to a physical or mental disability. The Social Security Administration, a physician, or Veterans Affairs can provide the needed certification. Our disability discharge program article covers recent automatic discharge expansions that have helped thousands of eligible borrowers.

Death Discharge. When a borrower dies, their federal student loans are discharged automatically upon submission of proof of death, such as a death certificate. For Parent PLUS Loans, discharge also applies if the student for whom the loan was taken out dies.

Pro Tip: If you believe you qualify for any of these programs, do not consolidate or refinance your loans before applying. Doing so can permanently disqualify you from receiving a discharge.

Now, let’s compare these options to the forgiveness pathways often mistaken for cancellation.

Cancellation vs. forgiveness: Comparing relief pathways

Cancellation can deliver immediate relief, but for millions of borrowers, forgiveness programs are the right path. The key is knowing which one fits your actual situation, especially given the significant changes that took effect in 2026.

Forgiveness programs most often confused with cancellation include Public Service Loan Forgiveness, or PSLF, which requires 120 qualifying payments while working full-time for a qualifying employer; Income-Driven Repayment forgiveness after 20 to 30 years of payments; and Teacher Loan Forgiveness of up to $17,500 after five years teaching at a qualifying low-income school.

These are earned through sustained effort over time. Cancellation, by contrast, applies the moment a qualifying event is confirmed.

Here’s what changed in 2026 and why it matters:

PSLF employer restrictions. A new PSLF rule, effective July 1, 2026, excludes employers with a “substantial illegal purpose,” including organizations that support terrorism or engage in certain prohibited immigration or medical activities. If you work for a nonprofit, confirm your employer still qualifies.

SAVE plan ended. The SAVE income-driven repayment plan has been discontinued and replaced by a new plan called RAP, which features a 30-year forgiveness timeline and an interest subsidy. If you were enrolled in SAVE, you need to take action and enroll in a qualifying replacement plan.

IDR forgiveness is now taxable. After 2025, IDR forgiveness is taxed as ordinary income under current federal rules. This is a significant financial shift that borrowers need to plan for now.

The numbers behind these programs are striking. As of March 2026, 21,200 borrowers received IDR forgiveness in a single month. Over one million total PSLF approvals were recorded by December 2024. And $17.2 billion has been forgiven through Borrower Defense alone.

“Knowing whether your situation calls for cancellation or forgiveness isn’t just a paperwork question. It’s a financial decision that can cost you years of unnecessary payments if you get it wrong.”

You can get details on how these programs work together in our PSLF and Teacher Forgiveness breakdown, and stay current on policy shifts through our Education Dept guidance updates.

Having compared relief paths, let’s outline how to navigate the loan cancellation application process.

Applying for loan cancellation: Step-by-step guidance and common mistakes

Applying for loan cancellation takes preparation. The process varies by program, but the foundation is the same: gather your documentation, submit the correct application, and follow up consistently.

Step-by-step application process:

Identify the right program. Determine whether your situation involves school misconduct, closure, disability, or death. Each program has a different form and different evidentiary requirements.

Gather your documentation. For Borrower Defense, this means enrollment records, marketing materials, communications from the school, and any evidence of the misrepresentation. For TPD, you’ll need medical certification. For Death Discharge, a certified death certificate is required.

Submit the correct application. Use the official Borrower Defense application on StudentAid.gov. Other discharge applications can also be found through your loan servicer. Do not use third-party services that charge fees to submit these free federal applications.

Request forbearance if needed. While your Borrower Defense application is being reviewed, you can request that your loans be placed in forbearance so payments are paused. Interest may still accrue, so weigh this carefully based on your situation.

Track your application status. Keep copies of everything you submit and note the dates. Follow up with your servicer every 60 to 90 days to check on the review status.

Respond promptly to any requests. The Department of Education or your servicer may ask for additional documentation. Responding quickly keeps your case moving forward.

Common mistakes to avoid:

Consolidating loans before applying. Consolidation can void your eligibility for Borrower Defense and Closed School Discharge. Always check program rules before making any changes to your loans.

Refinancing with a private lender. Private refinancing permanently removes your loans from the federal system, eliminating any discharge eligibility entirely.

Missing deadlines. Some programs have specific windows. Closed School Discharge eligibility, for example, depends on when you withdrew relative to the school’s closure date.

Falling for scams. Bad actors prey on confused borrowers. Be cautious of anyone promising guaranteed forgiveness for an upfront fee. Review our forgiveness scams guide before engaging with any outside service.

Pro Tip: Federal rules change frequently. Before you submit any application, visit StudentAid.gov or consult a qualified student loan advisor to confirm you’re working with current information. Our loan forgiveness future resource keeps you updated as policy evolves.

Now that you understand both the process and pitfalls, let’s share some perspective from years of student loan assistance.

Why loan cancellation often delivers faster relief—and what most borrowers miss

Here’s what we’ve noticed working with borrowers over time: cancellation is almost always underutilized. Most people arrive focused entirely on PSLF or IDR, and cancellation never enters the conversation. That’s a problem.

The loudest programs get the most attention. PSLF has over a million approvals and strong advocacy. IDR forgiveness is the default backup plan. But Borrower Defense and Closed School Discharge have quietly resolved billions of dollars in debt for borrowers who were wronged by their schools. The relief is real, it’s meaningful, and it’s available right now for those who qualify.

What concerns us most heading into the second half of 2026 is how the rule changes are creating new blind spots. The SAVE plan ending mid-cycle left many borrowers in limbo. The new RAP plan has a 30-year forgiveness timeline, which is longer than older IDR options. And the addition of IDR tax liability means some borrowers will face a large tax bill after decades of enrollment. These aren’t minor details. They change the entire math of your repayment strategy.

Our honest view is this: if you experienced any form of school misconduct, even years ago, it’s worth looking into Borrower Defense. If your school closed, even if you graduated shortly before, check the timeline. If you or a family member has a qualifying disability, the automatic TPD discharge expansion has made this easier than ever before. Don’t assume you don’t qualify. Actually check.

And if you’re in a forgiveness program, make sure your employer still qualifies under the 2026 PSLF rule changes. Don’t wait for your servicer to notify you. Take initiative, verify your status, and consult someone who knows the current rules. The student loan relief guide we’ve put together is a practical starting point.

Get expert help navigating loan cancellation and forgiveness

Understanding loan cancellation is one thing. Organizing your documents, submitting the right forms, and tracking your application status is another challenge entirely. At TitanPrep, we specialize in helping borrowers do exactly that. Our team assists with preparing and submitting applications for programs including Borrower Defense, Closed School Discharge, TPD Discharge, PSLF, and IDR plans. We also provide secure document storage and deadline tracking so nothing falls through the cracks.

Start with our forgiveness program guide to understand your options in plain language. Then explore how loan relief works with our support to see what the process looks like step by step. For quick answers to the most common borrower questions, our Student Loan FAQs page is a reliable resource. TitanPrep does not guarantee outcomes, but we do guarantee that you’ll be better organized and better prepared.

Frequently asked questions

Is loan cancellation the same as forgiveness for federal student loans?

No. Loan cancellation eliminates your balance because of a qualifying event like school misconduct or disability, while forgiveness is earned through public service or long-term repayment under an income-driven plan.

How do I qualify for Borrower Defense to Repayment?

You must show your school misled you or broke its contract, then submit a Borrower Defense application with supporting documentation; the Department of Education reviews your claim and can grant a full or partial discharge, though the process can take years.

Will IDR forgiveness be taxed in 2026?

Yes. Under current federal rules, IDR forgiveness received after 2025 is considered taxable income, so borrowers should plan ahead for the potential tax impact.

What happens if I consolidate or refinance my loans before applying for cancellation?

You may permanently lose eligibility for programs like Borrower Defense or Closed School Discharge, as consolidation and refinancing can void your discharge qualifications. Always verify program rules before making any changes to your loan structure.

Recommended

Student loan eligibility list: qualify for forgiveness and relief

Public Service Loan Forgiveness: Student loan relief will definitively end in January

The Future of Student Loan Forgiveness: What You Need to Know Before the Election Deadline

Finally! Glimmers of Hope for Student Debt Cancellation in 2022

Comments