PSLF guide: eligibility, steps, and staying compliant

- TitanPrep Official

- May 4

- 10 min read

Working in public service does not automatically mean your student loans will be forgiven. That is one of the most common and costly misunderstandings about the Public Service Loan Forgiveness program. Many borrowers spend years in qualifying jobs only to discover they were on the wrong repayment plan, had the wrong loan type, or missed a critical certification step. This guide walks you through exactly what PSLF requires, who qualifies, how to apply, and how to stay compliant as rules continue to change in 2026.

Table of Contents

Key Takeaways

Point | Details |

PSLF basics | Loan forgiveness is available after 120 qualifying payments while working full-time for an eligible employer. |

Employer eligibility | Check your employer’s eligibility regularly, especially with the new exclusions starting in July 2026. |

Payment tracking | Certify employment annually and keep detailed records to avoid missing PSLF credit. |

Rule changes | Stay current on political and regulatory changes affecting PSLF eligibility. |

Expert tips | Act quickly on loan consolidation and track compliance to help keep your records organized and reduce paperwork errors. |

What is Public Service Loan Forgiveness?

Public Service Loan Forgiveness, commonly called PSLF, is a federal program with a straightforward promise: work full-time for a qualifying employer, make 120 qualifying monthly payments, and the remaining balance on your eligible federal loans is forgiven tax-free. The program was established in 2007 to encourage people to pursue careers in public service by reducing the long-term burden of student debt.

But the details matter enormously. Not every federal loan qualifies. Not every payment counts. And not every public service job meets the program’s definition.

Which loans are eligible?

Only Direct Loans are eligible for PSLF. These include:

Direct Subsidized Loans

Direct Unsubsidized Loans

Direct PLUS Loans

Direct Consolidation Loans

If you have older Federal Family Education Loans (FFEL) or Perkins Loans, you are not automatically excluded. However, those loans must be consolidated into a Direct Consolidation Loan first. There is a significant catch: consolidation can reset your qualifying payment count to zero. So if you made 60 payments on an FFEL loan before consolidating, those payments do not carry over. Borrowers should verify how consolidation affects their count before acting.

This is a point where many borrowers lose years of progress. If you are unsure whether your loans are Direct Loans, log into studentaid.gov and check your loan types before making any decisions.

Common misconceptions

Many people assume that any government or nonprofit job qualifies. Others believe that any repayment plan works. Neither is true. PSLF has specific requirements for employer type, loan type, repayment plan, and payment timing. Missing any one of these can disqualify payments that you thought were counting.

It is also worth knowing that programs like teachers loan forgiveness are separate from PSLF. They have different rules and timelines. Pursuing both simultaneously requires careful planning. You should also be aware that the loan relief timeline has shifted significantly in recent years, making it more important than ever to stay informed. Past policy changes, including the limited PSLF waiver, temporarily allowed more payments to count, but that window has closed.

With the basics clarified, next we’ll help you understand who qualifies and what counts as eligible employment.

Who qualifies for PSLF? Employers, jobs, and hours explained

Qualifying for PSLF is not just about where you work. It is also about how many hours you work and what your employer does. Here is a clear breakdown.

Qualifying employer types

Qualifying employers include:

U.S. federal, state, local, and tribal government agencies

501©(3) nonprofit organizations (regardless of the services they provide)

Other nonprofits that provide certain qualifying public services, such as public health, public education, or law enforcement

For-profit companies do not qualify, even if they do work that benefits the public. Labor unions and partisan political organizations are also excluded.

Hour requirements

You must work full-time, which the Department of Education defines as at least 30 hours per week or your employer’s definition of full-time, whichever is greater. If you hold multiple part-time jobs at qualifying employers, you can combine hours to meet the 30-hour threshold.

The 2026 rule change and new exclusions

A final rule effective July 1, 2026 introduces a new category of excluded employers. Under this rule, organizations with a “substantial illegal purpose” will not qualify as PSLF employers. The Department of Education lists examples such as employers that aid illegal immigration, support certain medical procedures for minors, support terrorism, or show patterns of discrimination.

The Department will determine employer status based on a “preponderance of evidence” standard. Importantly, payments made before July 1, 2026 will still count even if your employer is later excluded. But payments made after that date at a disqualified employer will not count going forward.

Legal challenges to these exclusions are ongoing. Advocacy groups and some members of Congress have raised concerns that the rule could be used to target organizations serving immigrant communities or LGBTQ+ individuals. The situation is still evolving, so staying current on education department guidance is essential.

Key point: If you work at an organization that could be affected by the new exclusions, verify your employer’s status before July 1, 2026. Payments made before that date are protected.

Pro Tip: Before accepting a new job or submitting your first qualifying payment, use the PSLF Help Tool at studentaid.gov to confirm your employer’s eligibility. This one step can save you years of wasted payments. If you believe your employment situation has been affected unfairly, resources on education wrongful termination may also be relevant.

You may also want to review whether you qualify for other forms of relief. Check out DOE forgiveness eligibility to see if additional programs apply to your situation.

Knowing who qualifies sets the stage for understanding the payment requirements and plans needed for PSLF.

Qualifying payments and repayment plans for PSLF

Making 120 qualifying payments sounds simple. But the conditions around what makes a payment “qualifying” are strict. Missing even one requirement can disqualify that month’s payment.

Acceptable repayment plans

Qualifying repayment plans include:

Income-Based Repayment (IBR)

Pay As You Earn (PAYE)

Saving on a Valuable Education (SAVE)

Income-Contingent Repayment (ICR)

The standard 10-year repayment plan

The standard 10-year plan technically qualifies, but it is rarely the best choice for PSLF because you would pay off your loan in full before reaching 120 payments. Income-driven plans (IDR) are usually the better fit because they lower your monthly payment, leaving a larger balance to be forgiven.

What makes a payment qualifying?

According to federal guidelines, a qualifying payment must meet all of the following conditions:

Made under a qualifying repayment plan

For the full amount due as shown on your bill

No later than 15 days after the due date

Made as a separate monthly payment (lump-sum payments do not count as multiple months)

Made after October 1, 2007

Made while you are not in default on your loans

Common mistakes to avoid

Being on a graduated or extended repayment plan (these do not qualify)

Making extra payments thinking they will count as future months (they do not)

Missing a payment by even a few days and not realizing it was disqualified

Consolidating loans mid-progress, which resets your payment count

Pro Tip: The SAVE plan has faced legal challenges that have placed many borrowers in forbearance. Forbearance months do not automatically count as qualifying payments. Monitor your repayment plan status closely and check for updates on automatic PSLF forgiveness to understand how these changes may affect your count. The PSLF limited waiver guide also offers useful context on how past waivers affected payment counts.

With payments covered, let’s move to the step-by-step process for applying and maintaining eligibility.

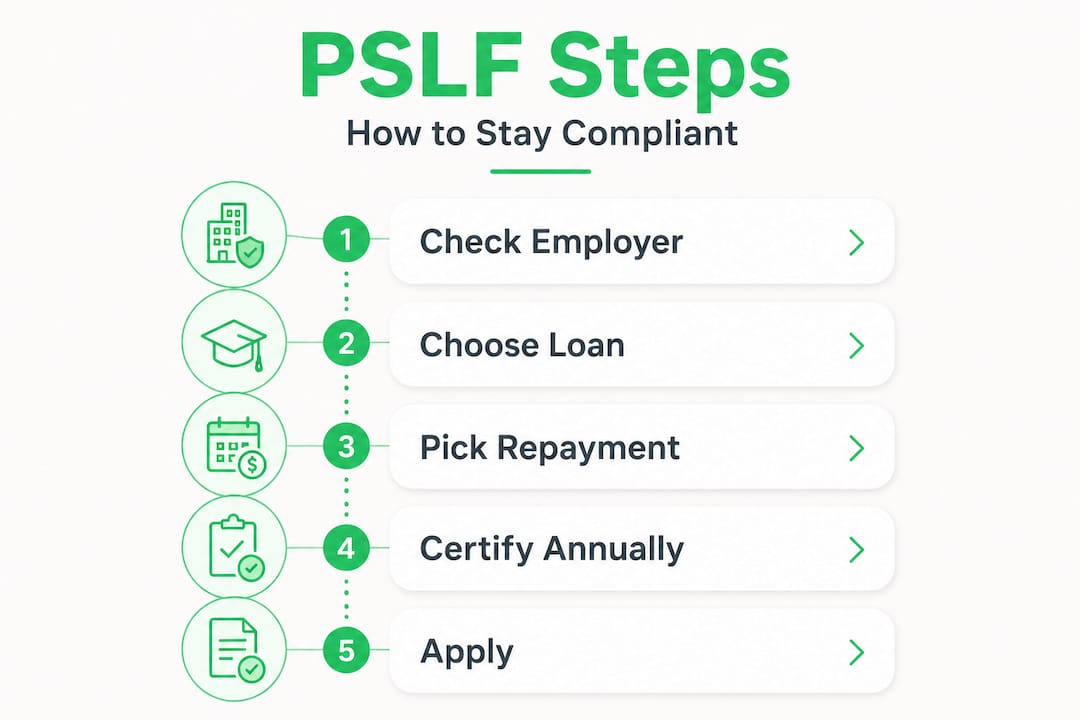

PSLF application process and compliance tracking

Applying for PSLF is not a one-time event. It is an ongoing process that requires annual attention and careful record-keeping throughout your entire repayment period.

Using the PSLF Help Tool

The PSLF Help Tool at studentaid.gov is your starting point. It helps you:

Check whether your employer qualifies

Generate the Employer Certification Form (ECF)

Submit the form digitally with your employer’s electronic signature

PSLF tracking is handled through Federal Student Aid/StudentAid.gov and the assigned servicer. Once your ECF is submitted, they review it and update your qualifying payment count.

Step-by-step application process

Confirm your loan type is a Direct Loan (or consolidate if needed)

Enroll in a qualifying income-driven repayment plan

Verify your employer’s eligibility using the PSLF Help Tool

Submit your ECF annually and whenever you change jobs

Monitor your qualifying payment count through studentaid.gov

After reaching 120 qualifying payments, submit the PSLF application for forgiveness

Compliance tracking best practices

Staying compliant means more than just making payments. You need to actively manage your records. Here is what to track:

Pay stubs and W-2s to confirm employment dates and hours

Copies of every ECF submitted and confirmation receipts

Records of all communications with your loan servicer

Screenshots or printouts of your payment count from studentaid.gov

Important: Log into studentaid.gov regularly to verify your payment count. If a payment is not counted correctly, catching it early gives you time to dispute it.

One additional option for borrowers who spent time in forbearance or deferment is the PSLF Buyback program. This allows you to make lump-sum payments to cover certain months that did not count. However, there is currently a backlogged for Buyback applications. If you are close to reaching 120 payments, the Buyback may not process in time to help you anyway.

Pro Tip: Keep a dedicated folder, either physical or digital, for all PSLF-related documents. Include your ECFs, payment records, employer contact information, and servicer correspondence. This folder could be the difference between getting forgiveness and losing credit for years of payments. For additional guidance on building your records, see preparing for PSLF success.

Also note that protections under FEHA protections for educators may be relevant if your employment situation changes due to discrimination or other workplace issues.

Now let’s address the political context, controversies, and what borrowers should watch out for as rules change.

Recent rule changes, political controversy, and staying compliant

PSLF has always existed in a politically charged environment, but 2026 has brought new tensions that borrowers need to understand.

The 2026 employer exclusion rule

As noted earlier, a final rule effective July 1, 2026 excludes employers with a “substantial illegal purpose.” The categories listed include:

The Department of Education will make these determinations on a case-by-case basis. Payments made before July 1, 2026 are protected even if an employer is later excluded.

Two sides of the debate

The current administration’s position is that the rule protects taxpayers from subsidizing activities that violate federal law. Critics, including Democratic lawmakers and advocacy organizations, argue that the rule is politically motivated and could be used to target nonprofits serving immigrant and LGBTQ+ communities. Several lawsuits have been filed to block the rule from taking effect.

What this means for you

If you work at an organization that could fall under these new exclusions, take action now. Payments made before the July 1, 2026 deadline are still protected. Review your employer’s status carefully and consult the PSLF program inquiry resources for background on how the program has evolved.

The safest approach is to verify your employer’s eligibility using the PSLF Help Tool before the rule takes effect, and to document your employment thoroughly in case you need to dispute a future determination.

Having explored the evolving landscape and risks, let’s think about what borrowers, experts, and advocates often overlook.

The uncomfortable truths most PSLF guides miss

Here is something most guides will not tell you directly: PSLF is not a passive program. It rewards borrowers who treat it like a project they actively manage, not a benefit they passively receive.

Most borrowers underestimate how much annual tracking matters. A single year of missed certifications can create gaps in your record that take months to resolve. Servicer errors are real and documented. If you are not checking your payment count regularly, you may not catch a mistake until it is too late to fix it easily.

The PSLF Buyback program sounds like a safety net, but the 27-month backlog means it is not reliable for most borrowers who are close to 120 payments. Do not count on Buyback to rescue missed months. Build good habits from the start instead.

The 2026 employer exclusion rule also creates a narrow but important window. If you work at an organization that might be affected, switching jobs or submitting payments before July 1, 2026 could preserve eligibility that you would otherwise lose. This is not about gaming the system. It is about understanding the rules well enough to protect yourself.

Finally, always verify your employer’s eligibility before you start counting payments. Borrowers have lost years of progress because they assumed their employer qualified without checking. The PSLF Help Tool exists for exactly this reason. Use it.

Pro Tip: Certification and record-keeping are not administrative chores. They are the foundation of your forgiveness claim. Treat every ECF submission and every payment record as evidence you may one day need to present. For a full overview of how to organize your federal loan documents, the federal loan guide is a strong starting point.

Get personalized support for your PSLF journey

Navigating PSLF on your own is possible, but it takes consistent attention and a clear system for staying organized. TitanPrep is a document preparation and support service that helps borrowers like you prepare and submit PSLF-related paperwork, track deadlines, and maintain records of submissions and communications with loan servicers.

Whether you need help organizing your ECF submissions, understanding recent rule changes, or preparing your application after reaching 120 payments, TitanPrep’s client portal gives you a secure place to upload documents and monitor your file. Visit student loan help to get started, download the loan forgiveness guide for a detailed overview of your options, and check student loan updates to stay current on the latest changes. TitanPrep does not guarantee outcomes. Eligibility is determined solely by the Department of Education or your loan servicer.

Frequently asked questions

What types of jobs qualify for PSLF?

Federal, state, local, and tribal government jobs and 501©(3) nonprofit positions qualify, but for-profit employers, labor unions, and partisan political organizations do not.

How often do I need to certify my employment for PSLF?

You should submit your ECF annually and any time you change jobs to keep your qualifying payment count accurate and up to date.

What happens to prior PSLF payments if my employer is excluded by new rules?

Payments made before July 1, 2026 still count toward forgiveness, but payments made after that date at a disqualified employer will not be counted.

Is consolidating loans required for PSLF?

FFEL and Perkins Loans must be consolidated into a Direct Consolidation Loan to become eligible, but this resets your qualifying payment count to zero.

How can I track my qualifying PSLF payments?

Log into studentaid.gov to view your current payment count, and keep thorough records including pay stubs, W-2s, and copies of every ECF you submit.

Recommended

Comments